Table of Content

If you’ve been on active duty for more than 90 days, you can qualify for a VA home loan. Unlike other types of veterans, you’ll need to demonstrate that you’ve served 90 days or more on active duty in to qualify for a VA home loan. In addition, you’ll need to prove that you’ve been on active duty for at least 181 days. Whether you’re a member of the National Guard, you can qualify for a VA home loan if you meet all of the other requirements.

The ability to purchase a home with the favorable terms of a VA loan is one such advantage. While there are no specific VA loans for national guard service members, national guards do qualify for the same VA loan as other military persons. Yes, you can get a VA loan if you served or are still serving in the National Guard or Reserves. Obtaining a VA loan as a Reservist or as part of the National Guard is very similar to regular military. The main difference is in the service requirements and the methods of verifying service and discharge status.

Can I get a Certificate of Eligibility for a VA direct or VA-backed home loan?

The requirements for the loan are a few and differ from state to state. The average VA Home Loan for a Reserve or National Guard service member is $310,000. You can get a mortgage if you have served for at least nine years. The National Guard and reserve can qualify for a VA Home Loan. To qualify, the applicant must have completed at least 90 days of service during a war and at least 181 days during peacetime.

If you meet the other requirements, you can still qualify for a home loan. National Guard troops who may have trouble qualifying for a conventional loan or coming up with the higher down payment often required with them will find their expanded VA loan benefit an attractive alternative. Similarly, members involuntarily separated from the Selected Reserve due to a deactivation of their unit between Oct.1, 2007, and Sept. 30, 2014, may receive a 14-year period of eligibility. Before you can obtain a VA loan, your lender requires proof that you are eligible. This proof comes from the VA in the form of a Certificate of Eligibility.

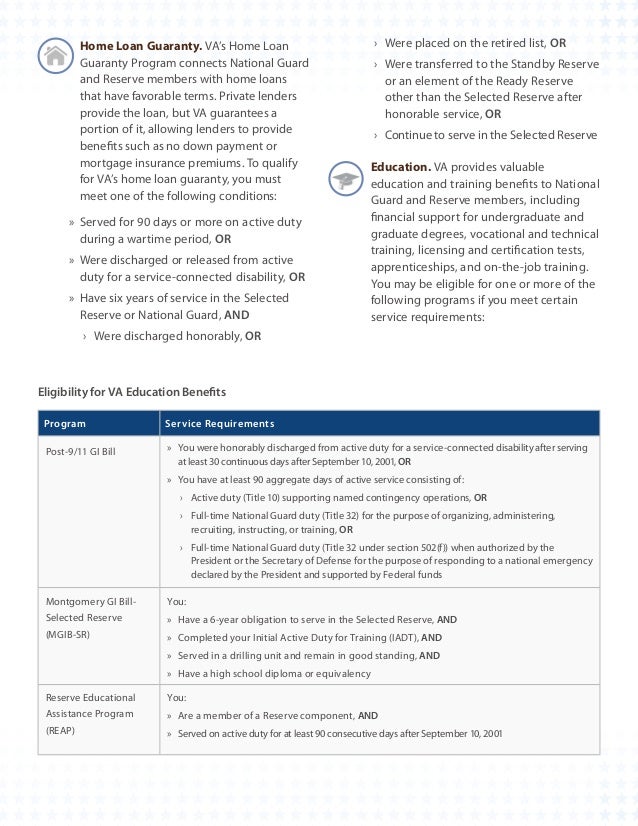

Reserve Educational Assistance Program (REAP)

You can get the Certificate of Eligibility through the US Department of Veterans Affairs here. There are also additional stipulations that National Guard or Reserve members must follow in order to become certified. These are just to ensure that you are eligible, and you meet any of the criteria, this step should not be an issue. To obtain a COE, you'll need proof of service and discharge. National Guard and Reserve members do not have one form to show proof of service like the DD Form 214, which is the proof of service for regular military . Before you buy, be sure to read the VA Home Loan Buyer's Guide.

Generally, all Reserve and National Guard members discharged or released under conditions that are not dishonorable are eligible for some VA benefits. The length of your service, service commitment and/or your duty status may determine your eligibility for specific benefits. Active Guard and Reserve members performing active service with pay from the Federal government may qualify for a variety of VA benefits. One thing to note is that active duty must be during wartime. If a National Guard member is active for State Active Duty, this time does not count toward the active duty requirement. However, National Guard members can still get additional benefits form the state, depending on the state they serve in.

Eligibility requirements for VA home loan programs

Another benefit of a National Guard VA home loan is its low interest rates. The interest rate is often much lower than other types of mortgages. A typical VA home loan will have an interest rate less than 0.25%, and you’ll be able to negotiate a lower rate. You must also make sure that you’ll be able to afford the house that you’ve chosen. If you’re planning to stay in the home for at least five years, you should check with the seller to find the perfect one. When it comes to cons of a National Guard VA home loan, the pros outweigh the cons.

The VA loan program provides a variety of benefits for eligible National Guard members. These benefits help veterans increase their buying power when searching for a home and enable them to save thousands of dollars over the life of their loan. The benefits of the VA loan program are available to eligible National Guard members for life. The minimum active-duty service requirements depend on when you served. Reservists who do not qualify for VA housing loan benefits may be eligible for loans on favorable terms insured by the federal Housing Administration , which is a part of HUD.

They lost eligibility if they went into the Inactive Ready Reserve . Members of the IRR called to active duty were eligible as long as they stayed in the IRR or Selected Reserve. OEF/OIF/OND Veterans may be eligible for a one-time dental evaluation and treatment following separation from service, if they did not have a dental exam prior to separation. Veterans must request a dental appointment within the first 180 days post separation from active duty. Activated Reservists and members of the National Guard are eligible if they served on active duty in a theater of combat operations after Nov. 11, 1998, and were discharged under other than dishonorable conditions.

Before sharing sensitive information, make sure you're on a federal government site. Get a Quote A VA approved lender; Not endorsed or sponsored by the Dept. of Veterans Affairs or any government agency. As the pandemic lingers, some of those Guard members are spending months taking care of communities across the country. Until now, many of them weren't eligible for a VA loan. These outreach teams are located at VAMCs to help ease the transition from military to civilian life.

In addition to our flexible, knowledgeable, and compassionate services, HomePromise proudly offers National Guard members a highly competitive loan origination fee. No matter the total loan amount or the type of loan, our HomePromise VA loan origination fee is $590. Do you need private mortgage insurance if you take the 0 down option? I’m curious; because if I don’t have to spend a ton on a down payment I’d rather put it toward something like remodeling a kitchen or something, but I dont want the extra money toward the insurance in my monthly.

At HomePromise, our mortgage experts are often asked if National Guard members are also eligible for VA loans. The answer is yes, as long as the National Guard member meets qualifying loan requirements and also meets the service requirements that are set forth by the Department of Veterans Affairs. You earned your home loan benefits through your national guard service.

No comments:

Post a Comment